Our view at Stack - Shopify has just about everything you need if you're looking to sell online. It excels with unlimited products, user-friendly setup, and 24/7 support. It offers 6,000+ app integrations, abandoned cart recovery, and shipping discounts up to 88%. Plus, it allows selling both online and in-person, scaling as your business grows.

In 1944, a Coca-Cola bottle exploded in Gladys Escola’s hand as she stocked shelves, giving her a severe five-inch cut. Her lawsuit against Coca-Cola Bottling Co. shaped modern US product liability laws.

Today, product liability remains a pressing concern for businesses. In this guide, you’ll learn the essentials of product liability insurance and how to protect your business.

What is product liability insurance?

Product liability insurance protects your business from legal claims of bodily injury or property damage caused by products you make, distribute, or repair. It safeguards you from costly lawsuits if your product unintentionally harms someone. While some cases of injury or damage are covered under general liability insurance, product liability insurance provides more comprehensive protection.

How much does product liability insurance cost?

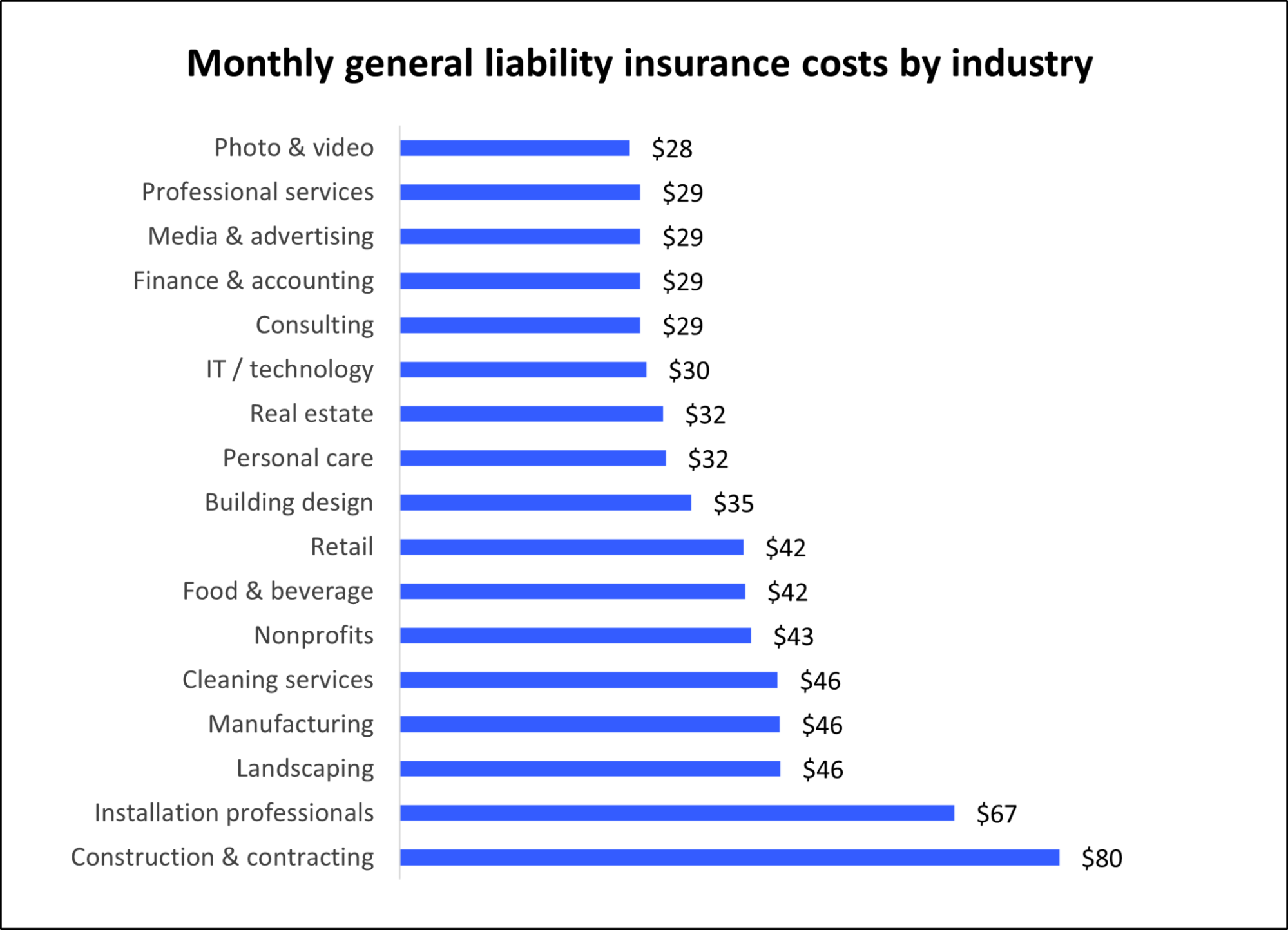

Product liability insurance costs vary depending on factors like your industry and coverage limits. According to AdvisorSmith, the average cost is about $99 per month or $1,192 per year. Insureon estimates a lower average of $42 per month, or $500 per year.

Rates could be higher for “riskier” products and lower for those considered less risky. For example:

- Nearly one-third of Insureon customers pay less than $30 monthly

- 41% pay between $30 and $60 per month

- Higher-risk industries may include food products, construction, and skin care

- Lower-risk industries often include photography, video production, and professional services

According to Insureon’s data, installation, construction, and contracting businesses pay the highest rates, while industries like photography, video production, professional services, and media and advertising typically pay less.

Your coverage plan and limit also factor into the cost. Most Insureon customers, for example, opt for a $1 million per-occurrence limit and a $2 million aggregate limit. This means the insurance covers up to $1 million for any single claim and up to $2 million for all claims during the policy period.

How does product liability insurance work?

If you make or sell products, your business can be liable for damages if your product harms a customer—even if they misuse it.

Product liability insurance protects you from potential legal and financial consequences:

This insurance provides third-party coverage, meaning:

- Payments for damages go to those affected or injured (the third party)

- Your business (the first party) is shielded from direct financial impact

What does product liability insurance cover?

Product liability insurance covers damages caused by specific factors:

- Design defects: Flaws in the product’s design.

- Manufacturing defects: Issues that occur during production.

- Marketing errors: Mistakes in marketing materials, such as incorrect labeling.

- Insufficient warnings: Lack of adequate warnings about potential risks.

- Strict liability: Harm caused by the product, even if you’re not at fault or it wasn’t intentional.

Product liability coverage does not include:

Product liability coverage provides financial protection for:

- Legal fees: When a customer sues your company for product-related injuries.

- Property damage: When your product damages a customer’s property.

- Medical expenses: If your product causes illness or injury.

- Wrongful death: If your product leads to someone’s death.

Who needs product liability insurance?

Product liability insurance is essential for businesses that produce, distribute, or repair physical products. Remember, the definition of “product” can be broad. For example, if you sell food products and someone gets sick from your food, you’ll want this coverage.

Consider product liability insurance if your company is in these industries:

- Manufacturing: Covers liability for products that cause bodily injury.

- Distribution: Protects against damages caused by defective products you distribute.

- Retail: Covers liability for the products sold, even if you don’t manufacture them.

- Food: Protects against claims related to food poisoning or allergic reactions.

- Construction: Covers electricians, general contractors, plumbers, and others for job site damage and injury.

- Beauty and cosmetology: Protects against allergic reactions and physical harm from beauty products.

- Repairs: Covers liability if someone is hurt due to your repair work, whether appliances, vehicles, or other products.

Types of claims covered by product liability insurance

Understanding the different types of claims is crucial for choosing the right product liability insurance coverage. The main types include:

Defective manufacturing claims

Defective manufacturing occurs when a product doesn’t meet its specifications. These claims focus on flaws in specific products rather than the overall design. Usually present in a small percentage of items, examples include:

- Food products contaminated with foreign substances during production

- A bicycle with a cracked frame due to improper welding

Customers must prove the product was defective when it left the manufacturer’s control.

Design defect claims

These claims argue that a product’s design is inherently dangerous or defective, making the entire product line potentially hazardous for consumers, even if manufactured correctly. For example, children’s toys with small parts that pose choking hazards. Design defect claims can lead to large-scale product recalls and significant legal liabilities.

Inadequate instructions or warnings

These claims arise when a properly manufactured and designed product is deemed defective due to a lack of clear instructions or warnings about its use. For instance, if you sell power tools without proper safety precautions or operational guidelines, you could be liable for injuries caused by foreseeable misuse.

Breach of warranty claims

Breach of warranty occurs when a product doesn’t meet the promises or guarantees made by the manufacturer or seller. Two types of warranties are typically covered by insurance:

- Express warranties: Specific promises about performance, durability, or features, made in writing (e.g., manuals, packaging) or verbally (e.g., salesperson statements).

- Implied warranties: Automatic product guarantees, such as fitness for ordinary use (e.g., a refrigerator keeping food cool and lasting a reasonable time).

These claims may be easier for consumers to prove, as they only need to show the product didn’t meet warranty terms. Comprehensive product liability insurance can cover the costs of product replacement or repair under warranty.

Strict liability claims

Under strict liability, manufacturers and sellers are responsible for harm caused by defective products, regardless of whether they exercised reasonable care or the consumer was negligent. Many US states have adopted strict liability for product defects.

Customers can sue for manufacturing, design, or warning defects under strict liability without proving manufacturer negligence. This differs from other types of claims where negligence must be proven.

Negligence claims

Negligence claims arise when manufacturers, distributors, or sellers fail to exercise reasonable care in designing, producing, or selling a product. This falls under the duty of care, a legal obligation to protect customers. It includes the duty to:

- Design and manufacture safe products

- Adequately test products before release

- Provider proper warnings and instructions

- Inspect for defects and maintain quality control

- Stay informed about product safety and potential hazards

Customers may be eligible for compensation if they can prove negligence.

The importance of product liability insurance for small businesses

Product liability insurance is crucial protection against financial lossesfor small businesses operating on tight margins. Without it, a single product liability claim could lead to bankruptcy.

Product liability insurance covers various potential issues, from design defects to negligence. For example:

- A small electronics company produces a device that overheats and causes fires

- A local bakery’s products lead to food poisoning

Product liability insurance would cover legal fees, settlements, and other related costs in these cases.

While product liability insurance is often included in general liability policies, high-risk products may require a standalone policy. Consult your insurance provider to ensure you have adequate coverage.

How to get product liability insurance

To secure the best product liability insurance for your business:

- Request quotes from multiple insurance providers for comparison. Ask business contacts for referrals or start with a Google search.

- Check if you’re already covered. Your general liability insurance might provide sufficient product liability coverage. Review your existing insurance package to determine if you need additional coverage.

- Choose the correct coverage limit. Consider both the amount of coverage and the geographical areas where you’re protected.

- Consider bundling with a business owner’s policy (BOP). A BOP often includes product liability insurance, general liability, commercial insurance, and workers’ compensation. Coverage varies by insurance company and industry, so verify what’s included.

- Negotiate. Don’t hesitate to negotiate better rates or coverage policies before signing the contract.

Protect your business

Product liability insurance is essential for safeguarding your business. While accidents are infrequent, being prepared can provide peace of mind and allow you to focus on growing your business.

Product liability insurance FAQ

What insurance do I need to sell products?

Product liability insurance is essential. Consider general liability insurance as well.

Do I need business insurance if I sell online?

Yes, if you sell physical products. For digital products like software or web design, consider errors and omissions or professional liability insurance instead.

Do wholesalers need product liability insurance?

Yes, wholesalers should have product liability insurance.

Is product liability included in general liability insurance?

Some general liability policies include product liability insurance, but it’s not guaranteed and may not provide sufficient coverage for your needs.

Who should have product liability insurance?

Product liability insurance is recommended for:

- Manufacturers

- Wholesalers and distributors

- Retailers

- Importers

- Product designers

- Companies that assemble or install products

If Shopify is of interest and you'd like more information, please do make contact or take a look in more detail here.

Credit: Original article published here.