Our view at Stack - Pipedrive is a robust CRM platform, offering automation, contact data collection, webhooks, AI-powered sales assistant, email communications, email marketing, and customisable sales pipeline workflows.

Effective inventory management enables businesses to track stock levels, ensuring they never miss sales opportunities and avoid the pitfalls of overstocking.

In this article, you’ll learn why it’s worth tapping into inventory management for your small business. You’ll discover popular inventory management methods, how to adopt one that suits your business and best practices you can apply to make your inventory process more efficient.

What is inventory management?

Inventory management is the strategic process of overseeing your inventory across the supply chain. It’s about balancing incoming and outgoing items, but it’s also about planning and forecasting sales.

Inventory management enables you to have what you need when you need it and know where it is.

Your assets (like buildings and equipment) represent static cash because they’re long-term investments. Inventory, on the other hand, represents cash that flows in and out.

Inventory can fit into any of the following categories:

-

Raw materials. Unprocessed materials you can use to create finished goods. You generally source raw materials from suppliers (e.g., plastic, fabrics and wood).

-

Work-in-progress (WIP). Products that are partially processed but not finished. The less time your products spend in this phase, the more efficient your production process is.

-

Finished goods. Products that are ready for your customers. Since finished goods represent sales, having too many in your inventory means you have cash tied up.

-

Maintenance, repair and operating supplies (MRO). Products that support production and operations but aren’t part of your finished goods (e.g., cleaning supplies, light bulbs, office supplies).

Note: People often mistake inventory management for inventory control. While these terms have common ground, inventory control only focuses on tracking stock levels in your warehouse. Inventory management is a broader term that involves selling, ordering, storing, planning and keeping track of inventory levels.

How does inventory management work?

The supply chain is the network of people, processes and resources that transform raw materials into finished goods and delivers them to customers. Inventory management is a strategic component of supply chain management, ensuring products flow efficiently.

Here’s how the inventory management process typically works:

|

Process |

Example |

|

Planning involves analyzing historical data to look for trends or patterns. It helps you determine how much and how often you should order a product. |

Imagine you own a small coffee shop. According to historical data, you sell 100 pounds of Colombian beans monthly. During the holiday season, you know your sales increase to 150 pounds because of gatherings and gifts – so you need to stock accordingly. |

|

Purchasing starts when it’s time to restock. It involves identifying reliable suppliers to deliver your goods within a specific timeframe. |

After checking your inventory, you realize you’ll run out of Colombian beans in two weeks. From planning, you already know you’ll need 100 pounds of these beans each month. In this stage, you’ll need to choose a supplier that can deliver in two weeks or less. |

|

Storage is the process of putting away the products you receive from suppliers. Proper storage saves you time and improves efficiency as you know exactly where everything is. |

When the shipment of Colombian beans arrives, your staff will inspect the product to ensure it matches the quality standard agreed upon by your supplier. After documenting this, your staff will adequately label and store the beans so you know exactly where they are and if they’re close to their expiration date. |

|

Selling is about understanding your demand to ensure you can fulfill orders without running out of products. |

From tracking your sales, you know your average daily sales are four bags of Colombian beans. With that in mind, your staff will move this number of bags to the front. With a point-of-sale system that connects directly to your inventory, your inventory stock levels will automatically update with each sale. |

|

Monitoring regularly helps you change your strategy and make improvements. When you analyze your inventory performance over time, you can reduce costs and see where your money is tied up. |

Your inventory tracking shows that Colombian beans frequently run out of stock, meaning you should increase their order quantities. Meanwhile, Ethiopian beans sit longer on shelves and often spoil, so you should decrease their order quantities. |

Benefits of inventory management

Effective inventory management brings valuable advantages to businesses, impacting everything from your finances to customer loyalty. Here’s how it can make a difference:

-

Improved cash flow: knowing where your inventory is and for how long helps you understand if you have tied capital that can increase your cash availability. A study from Unleashed found that the average firm holds USD$142,000 of stock above what they’d need that year. Excess inventory ties up cash that you can use more effectively elsewhere.

-

Reduced costs: inventory management helps you identify what products generate unnecessary costs. The costs of keeping inventory in stock range between 15% and 30% of the inventory’s value. You’ll prevent money losses at these rates if you avoid holding onto unsaleable inventory for months.

-

Better decision-making: inventory management gives you the visibility to manage your small business effectively. You can identify trends and prepare for seasonal sales. Recognizing your bestsellers and underperforming items will increase your profit margins.

-

Customer satisfaction: customers expect reliability and convenience, with 91% of consumers less likely to buy from a business again after a negative experience such as a stockout. Proper inventory management ensures no shortage of inventory to fulfill demand.

Recommended reading

A beginner’s guide to customer experience

7 inventory management methods

An organized business is a successful business. Choosing an inventory management method is crucial to maximize your company’s efficiency.

Here are seven of the most popular inventory management methods for small business owners.

1. First-In, First-Out (FIFO) or Last-In, First-Out (LIFO)

FIFO assumes that you sell products in the order they arrive. In other words, you sell the oldest items in inventory first.

In the supply chain, the cost of labor and materials constantly changes due to inflation. FIFO is an effective method to ensure the best cost/value ratio as it assumes you bought older products at a lower cost. When you sell them first, the inventory left is closer to market value.

LIFO assumes you sell the newest products first, which can result in inventory staying in your warehouse indefinitely.

However, LIFO can lower companies’ taxes when prices rise. The last-in units are usually more expensive than the first-in units. That translates to a higher cost of goods sold (COGS) but less profit, which allows companies to cut taxable income.

When should you use FIFO or LIFO?

Using FIFO or LIFO depends on your strategy rather than your product type. You can choose FIFO to maintain freshness and market value or LIFO if saving on taxes during inflation is your priority.

While you can adopt either method, businesses often use FIFO for perishable products (e.g., beauty products, groceries, food), and LIFO is more common in non-perishable industries (e.g., hardware, retailers).

2. Just-In-Time (JIT)

JIT is a method in which you get the exact items you need when you need them. Its main goal is to reduce the inventory you keep at all times.

Inventory that stays in your warehouse for too long occupies space you could use to store high-turnover products (i.e., products that sell faster). The cost of keeping old products in your inventory is called holding cost.

With JIT, you minimize holding costs and increase inventory turnover. However, you must ensure accurate demand forecasting and carefully track your inventory for this method to work.

When should you use JIT?

JIT is best for businesses with predictable demand (e.g., manufacturing, auto parts, hardware). The key to using JIT is to have reliable or backup suppliers and a contingency plan in case they fail to deliver.

3. ABC analysis

The ABC analysis is an inventory management method based on the Pareto principle. It states that 80% of a company’s profit comes from 20% of its products.

The ABC analysis categorizes items into three groups based on their importance and impact on revenue:

-

A products (20% of inventory) are your most important items, accounting for 80% of your sales

-

B products (30% of inventory) are moderately important, accounting for 15% of your sales

-

C products (50% of inventory) are less important, accounting for 5% of your sales

You’ll find different breakdowns across sources, but the main point is that A products are your high-value items – even if they’re in smaller percentages than others.

ABC analysis helps you focus on the items that matter for your business. It also gives you more control over your inventory and aids your decision-making.

When should you use ABC analysis?

Use ABC analysis if you have multiple product lines and a predictable demand (e.g., healthcare, manufacturing, retail).

4. Economic Order Quantity (EOQ)

EOQ is a method for calculating the optimal quantity of units needed to meet demand and minimize inventory costs.

It comes with a formula:

EOQ = √ (2DS / H)

Where:

D is the annual demand (units per year)

S is the ordering cost ($ per order)

H is the holding cost ($ per unit per year)

For example, if your annual demand (D) is 1,000 units, the ordering cost (S) is $20 per order and the holding cost (H) is $3 per unit per year, this is how you determine your EOQ:

√ (2DS / H)

√ [(2 x 1,000 x 20) / 3]

√ 13,333.33

= 115.47 ≈ 116

An EOQ of 116 means this is the quantity you should order to minimize holding costs.

The EOQ formula assumes that your demand, fixed costs and lead time are constant – which isn’t realistic. However, EOQ is a good starting point for rough estimates and a baseline for more complex models.

When should you use EOQ?

You should use EOQ if your business experiences high volume, repetitive orders and stable business operations.

Recommended reading

How to forecast demand for a scaling financial services business

5. Par levels (min/max)

Min/max is one of the simplest types of inventory management. It attempts to keep inventory within a range of safety stock (the minimum) and excess stock (the maximum).

When the amount of inventory drops to the minimum level, your point of sale (POS) system or software sets an order to return it to the maximum level.

While the min/max method ensures consistent stock levels and clear reorder triggers, it’s not ideal for variable demand.

When should you use the min/max method?

You should use the min/max method if you have limited storage and predictable demand.

6. Perpetual inventory management

Perpetual inventory management uses inventory software to track your inventory in real time.

Perpetual inventory eliminates physical inventory checks as everything occurs within the system. When your employees process items (from sales, returns or restocking), the system automatically updates your inventory.

For this inventory management method, you’ll typically need:

-

POS systems

-

Barcode scanners/RFID

-

Software to manage inventory

-

Integration with accounting

-

Mobile devices for scanning

Perpetual inventory management lets you integrate data with other departments and support agile sales operations. Accounting teams, for example, will have access to real-time accurate data, which makes financial reporting and COGS calculations easier.

When should you use perpetual inventory management?

Perpetual inventory management is a recommended option for multi-location businesses or online sellers. It helps coordinate inventory and guarantee order fulfillment with real-time tracking across locations.

7. Consignment inventory

Consignment is a popular inventory management technique for new small businesses. It involves you (the consignor) supplying your product to a retailer (the consignee) to stock and sell in their location.

With consignment, you don’t have to pay for inventory costs until your product sells. The retailer takes on the risk and costs of displaying your product at their store.

If the product sells, the consignor and consignee split the revenue based on a previous agreement. If the product doesn’t generate sales in a specific period, the retailer returns your items to you.

When should you use consignment inventory?

Use consignment inventory if you’re a small business with limited capital. The technique works particularly well in the fashion industry, where inventory costs can add up owing to rapidly changing sales trends.

It’s also ideal for snacks and baked goods, where you can test small batches in different locations without investing in your own store.

Download Your Guide to Sales Performance Measurement

The must-read guide for any sales manager trying to track, forecast and minimize risk. Learn how to scale sales with data-backed decisions.

3 best practices for inventory management

Good inventory management starts with tracking your data, standardizing your inventory organization and having a tool that integrates all this information. These three core steps will help you as you work to cut costs or accurately predict demand.

Here’s how to follow these three best practices for proper inventory management:

1. Track and audit your inventory data

Tracking your inventory is essential to have constantly accurate data on your stock levels and improve your cash flow.

Think of your inventory as money sitting on your shelves. You need to track it properly to avoid finding expired products, running out of your bestsellers and making emergency orders with higher fees.

When tracking inventory, you should be able to answer three questions:

-

“How much should I order?”

-

“When should I order?”

-

“How long will it take to get here?”

To calculate accurately, monitor high-level metrics such as demand, current stock levels and lead time.

There are two other metrics you can use to improve your cash flow and understand your sales velocity:

-

Inventory turnover rate. This rate is how often you sell or replace your entire inventory in a specific period. It helps you understand how quickly you’re selling products. For example, if your turnover rate in one year is four, you’re replacing your inventory quarterly.

-

Stockout rate. This rate is how often you run out of inventory your customers want to buy. Stockout shows whether you’re meeting customer demand and properly managing your inventory. For example, if 5 of your 20 products went out of stock during a month, your stockout rate is 20%.

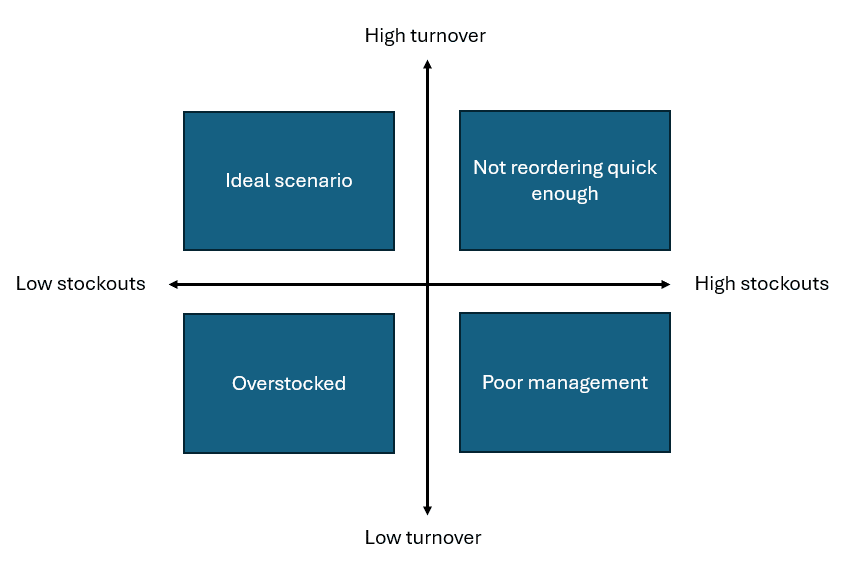

With these two metrics, you can draw the following conclusions:

-

High turnover and high stockouts mean you’re selling fast but not reordering quickly enough

-

Low turnover and low stockouts indicate you have overstock but never run out

-

High turnover and low stockouts mean you’re selling fast and meeting demand (ideal scenario)

-

Low turnover and high stockouts show you’re not selling nor meeting demand (poor inventory management)

Tip: You should do a manual inventory count at least once a year, even if you have inventory management tools that avoid discrepancies due to human error. Some businesses check their inventory monthly, and others daily for their most important items.

2. Have a protocol for receiving inventory

Receiving products from a supplier is a critical process affecting all business operations. A good receiving process can help you find products faster, avoid stockouts and improve your financial health.

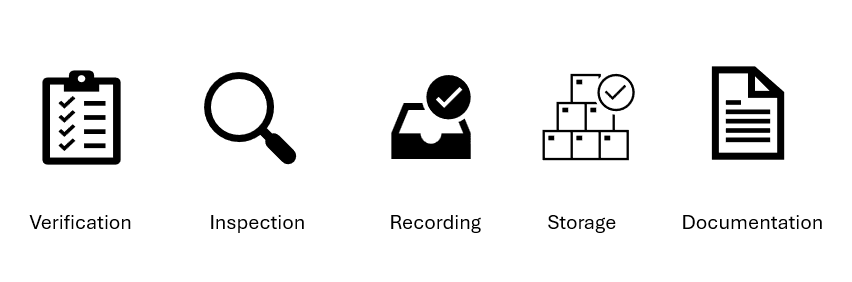

Your receiving process should have the following steps and protocols:

Verification

When you receive your products from a supplier, ensure someone on your end has a physical or digital copy of your order.

Having someone check the order minimizes errors, immediately verifying whether your supplier sent the right product in the correct quantities.

Inspection

Once your products are inside the warehousing area, look for damaged items or do a quality check. If you find anything that doesn’t match your product standard, document it and inform the supplier.

Recording

Using barcodes is good practice while you unpack your product. You should scan barcodes:

-

From each unit you receive

-

From each bin or pallet that you fill with units

-

From each location that you store your bin or pallet later on

If your supplier doesn’t provide products with barcodes, label them first. Recording is an essential step to update your inventory system and ensure accuracy.

Storage

Move each bin or pallet to its designated location. Remember to scan the location’s barcode to know exactly where each product is.

Documentation

Have a receiving log in place with the following information:

-

Time and date of the delivery

-

Name of the person (or group) receiving the order

-

Description of items received

-

Quantity of items received (pallets and units)

-

Condition of items

-

Storage location

-

Name of the person delivering the order

A receiving log ensures that if there’s an issue or the number of products doesn’t add up, you can find where the error is.

3. Invest in inventory management software

As you scale and add more product lines, you’ll need an inventory management system to help you track, order and analyze your stock.

Here are the features you should look for:

-

Forecasting. Estimates the number of products you’ll need each month (or period) and helps you predict sales by analyzing past trends or seasonality. For example, if a product is trending, the system will suggest increasing the following month’s order.

-

Inventory control. Tracks your current stock levels and expiration dates. You can scan items as they arrive, and this feature will update the system’s quantities.

-

Order management. Handles the process of ordering and purchasing inventory. You can either create purchasing orders or set reorder rules. If your inventory reaches the minimum level, the system automates an order.

-

Reporting/analytics. Provides all the information you need for better decision-making. You can view your products’ performance, sales data and cost analysis. The feature usually has a dashboard that lets you see which products are bestsellers and which tie up capital.

Tip: A quick Google search will give you multiple inventory management software options. If you’re still growing, concentrate on inventory management systems designed for small businesses. You can also check popular software marketplaces such as Capterra and G2 for a consolidated list of solutions with user reviews.

Best inventory management software

To further explore the best practice of investing in inventory management, here are the top inventory management software for small businesses we recommend:

1. Pipedrive

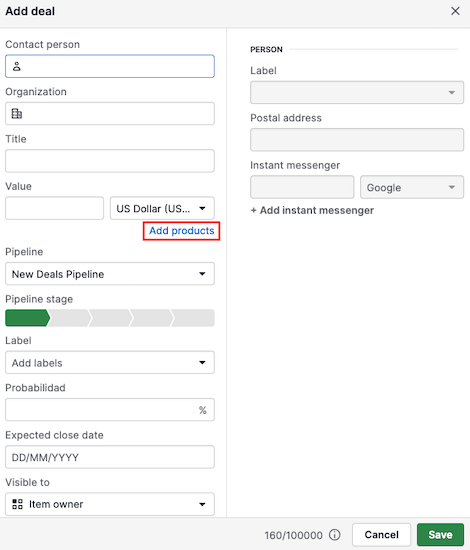

Pipedrive’s all-in-one customer relationship management (CRM) solution comes with a Products feature that allows you to create a catalog of products.

You can add products to a sales deal to help you keep track of potential sales.

When entering new deals into your Pipedrive account, you can use the “Add deal“ window to include new products.

Once you save a product, you can refine your entry by editing fields such as category, description, product code, price, tax, etc.

Key features

-

Add different product categories and prices in different currencies

-

Include tax percentages, discounts or promotions

-

Import product data from existing spreadsheets into Pipedrive

-

Link products to deals to have better visibility of potential sales

-

Multiple price points with distinctive names for the same product

Who should use Pipedrive?

Pipedrive is suitable for small businesses up to enterprise companies. It’s especially useful for made-to-order small businesses and those that need multiple pricing options (e.g., standard or premium products.)

Pipedrive is a sales tool, so it can also help organize your sales process (e.g., tracking closed and likely sales, forecasting sales for predicting future stock, etc.). It’s a powerful CRM with many built-in features and add-ons for when you need them (like email marketing).

Pipedrive also sits comfortably in your tech stack, with hundreds of Marketplace integrations that expand its inventory management capabilities and beyond.

Recommended reading

CRM vs. ERP Software: Which system is best for your business?

2. MRPeasy

MRPeasy is a software for production planning and inventory management. It helps you turn customer orders into manufacturing orders while optimizing stock levels.

Integrating this tool with Pipedrive’s CRM allows you to sync your sales efforts to manufacturing.

Key features

-

Production management to schedule and plan manufacturing operations

-

Gantt chart to keep track of day-to-day activities

-

Real-time data inventory quantities

-

Customer orders in which you can calculate prices and lead times

-

Integration with other tools (e.g., CRM, accounting, e-commerce)

Who should use MRPeasy?

Small to medium businesses focused on manufacturing or distribution.

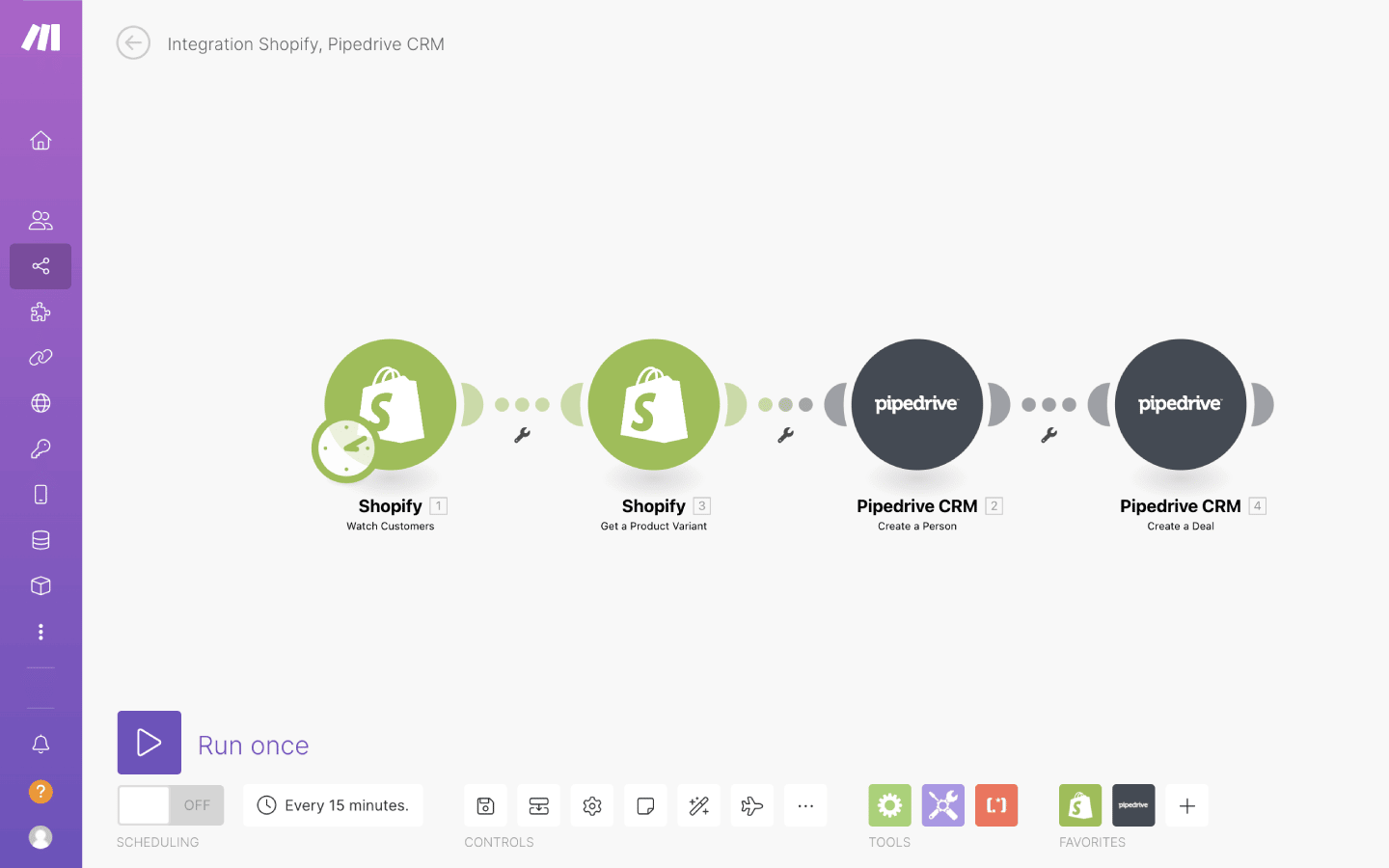

3. Shopify

Shopify is an e-commerce platform that helps businesses create and run an online store. Its inventory management system lets you track products across all your sales channels.

You can integrate Shopify with Pipedrive’s sales CRM to consolidate and streamline all data for your sales team.

Key features

-

Real-time tracking, alerting you when product quantities are running low

-

Reporting for specific periods

-

Multi-location management to monitor stock levels across different warehouses

-

Customer purchase history to understand your audience preferences

-

Integration with Pipedrive so your sales team has up-to-date information

Who should use Shopify?

Small to medium retail businesses or online stores.

Final thoughts

Inventory management is more about the process itself than the software or system enabling it. Keeping track of your product portfolio becomes easier when you have defined steps for managing your inventory that you can implement for your staff.

To ensure your company’s inventory management optimization across the board, apply the above methods and best practices, choose software that meets your needs and stay organized to be at the top of your game.

If Pipedrive is of interest and you'd like more information, please do make contact or take a look in more detail here.

Credit: Original article published here.