Our view at Stack - Shopify has just about everything you need if you're looking to sell online. It excels with unlimited products, user-friendly setup, and 24/7 support. It offers 6,000+ app integrations, abandoned cart recovery, and shipping discounts up to 88%. Plus, it allows selling both online and in-person, scaling as your business grows.

As a business owner, you know revenue is the amount you earn when you sell your product or service.

But what happens if a customer pays you in advance? You get the cash but have done nothing to earn it. This is where deferred revenue comes in.

Ahead, you’ll learn the basics of deferred revenue and how it works in accounting for your business.

What is deferred revenue?

In business, a customer sometimes pays for a service they will receive six or even 24 months later. So, you have the cash, but you haven’t performed the service or delivered any product yet.

Deferred revenue is the money a business receives from a customer for future services or products. Think of purchasing a gift card.

Imagine you purchase a $100 gift card from your favorite bookstore. The store collects your $100, but hasn’t sold you any books. The bookstore will record the $100 as deferred revenue until you redeem the gift card.

Accounting rulesdon’t allow the store to recognize the entire $100 as revenue because it has done nothing to give it a legitimate claim to that money.Even if not explicitly stated, business transactions are contractual with duties and rights for each party.

In the above example, the store has a duty to sell books to you and then has a right to the cash in on your gift card after giving you the books. The cash you receive before providing a service or delivering a product is called deferred revenue. You can also think of it as postponed revenue or unearned revenue.

How deferred revenue works in accounting

A set of accounting principles define how transactions are recorded in a company’s books of accounts. There are ten accounting principles and the revenue recognition principle is the most relevant for deferred revenue.

According to the revenue recognition principle, revenue is recorded when it’s earned, regardless of when the cash payment is received. For example, assume a SaaS company sells a two-year software license and receives $100,000 as full payment. The company can’t immediately recognize $100,000 upfront as revenue because it hasn’t earned it.

Instead, it recognizes revenue bit by bit as it delivers the software service over the two-year period.The company will record $4,166 in revenue ($100,000 ÷ 24 months) each month for the two-year licensing period.

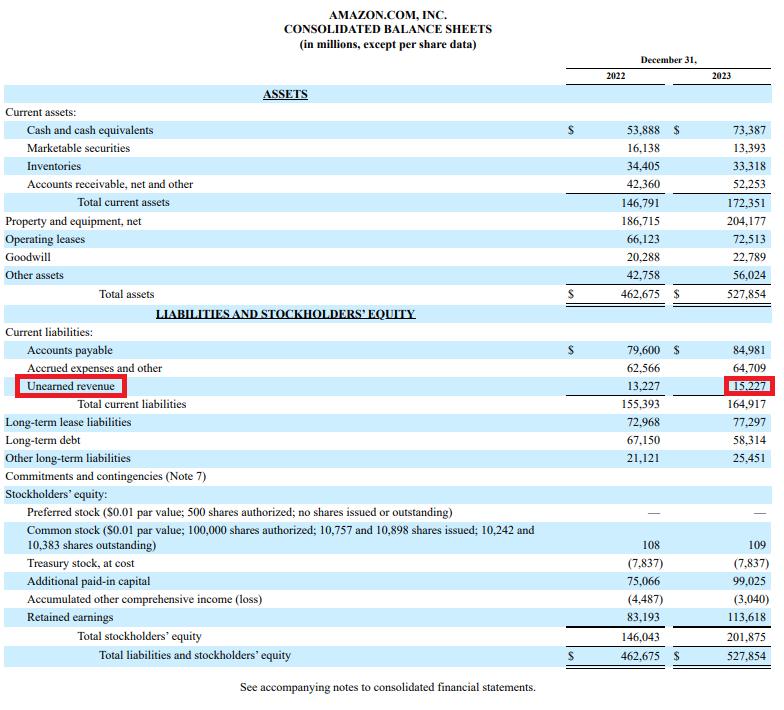

Businesses must record any advance cash payments as deferred revenue until they earn them by providing the service or delivering the product. Take a look at Amazon’s December 31, 2023 Balance Sheet.

Ignore all the words and numbers and only look at the items surrounded by red boxes.

On December 31, 2023, Amazon had $15.2 billion in unearned (deferred) revenue. As you read further through Amazon’s annual financial report, you learn that its unearned revenue is the following:

Deferred revenue vs. accrued revenue

There is a subtle difference between deferred revenue and accrued revenue. Remember that deferred revenue occurs when a business receives cash, but hasn’t provided a service or delivered a product.

Accrued revenue is the opposite of deferred revenue. It’s when a business hasn’t received payment for goods or services already provided. Another one of the 10 fundamental accounting principles is the accrual principle.

According to the accrual principle, transactions are recorded in the books of accounts when expenses are incurred or revenue earned, regardless of when cash exchanges hands. For example, you record salary expenses when you have an obligation to pay, not when you direct deposit paychecks to your employees’ bank accounts.

Similarly, you record revenue when you give a customer a product as agreed, not when you receive the cash. Accrued revenue is the same thing as accounts receivable. It’s when a customer owes you money. You shouldn’t omit these amounts from your financial books.

The same holds for expenses. Don’t leave them out of your financial statements. Assume, for example, that a business hasn’t paid salaries for a month. When the business closes its books at the end of the month, it needs to recognize the unpaid salaries as an expense and a liability.

How deferred revenue affects financial statements

Revenue is an income item and shows on the income statement. How about deferred revenue? In accounting, deferred revenue affects the financial statement differently because it is a liability, not income.

Here’s the reasoning.

The cash you receive for a service you haven’t provided is technically not yours. You’re keeping it in trust. It will pass to you only when you earn it. And circumstances can change, especially before you perform the agreed-upon service.

For example, let’s say a customer paid you$10,000 for a two-year SaaS software license. What happens when the next morning the customer changes their mind or experiences a significant business disruption and requests a refund?

Of course, you can flash a no-refund policy and keep the cash. But you did nothing to deserve the cash and therefore, should be obligated to pay it back.

Somehow, accounting captures this sense of natural justice by stating that deferred revenue should be recognized as a liability, not income. Once you’ve delivered the service or product paid for in advance, the deferred revenue liability disappears. You then record that amount as revenue.

How to manage and track deferred revenue

The best way to manage and track deferred revenue is with a revenue recognition schedule. This schedule captures the total initial advance payment, and then gradually reduces the amount as the business performs the agreed-upon service.

Suppose you have a customer who signs a 12-month contract for $12,000 on January 1. The contract has a recurring quarterly fee of $3,000.

Your revenue recognition schedule will look like this:

| Period | Revenue Recognized to-date | Deferred Revenue Balance |

|---|---|---|

| January 1 | $0 | $12,000 |

| March 31 | $3,000 | $9,000 |

| June 30 | $6,000 | $6,000 |

| September 30 | $9,000 | $3,000 |

| December 31 | $12,000 | $0 |

Knowing the deferred revenue portion can help prevent overspending because it represents future service delivery commitments and potential refunds. Plus, tracking deferred revenue can help businesses create more accurate and realistic cash flow predictions to plan for things like staffing needs and marketing initiatives.

Tracking deferred revenue means more accurate financial statements. Imagine in the above example that the company signed the 12-month contract in December, and the company recorded the entire $12,000 as revenue in December.

That means December revenue is inflated, and the company will show no revenue for the following year. Today, technology has made managing and tracking deferred revenue a lot easier.

Most accounting software has revenue recognition features that update deferred revenue in real time. These accounting systems provide charts, graphs, and tables breaking down revenue by month, showing what the company has earned and what’s still deferred.

Risks with deferred revenue

It may look simple, but deferred revenue comes with a set of risks businesses should be prepared to navigate. How you manage some of these risks can improve the financial health of your business or make a customer somewhere happy and satisfied.

The following are some common risks associated with deferred revenue.

Cash flow management challenges

One of the most common risks with deferred revenue is cash flow management. Consider a company that receives a large sum of cash from a customer at the start of the year for a one year software implementation project.

But the company uses all of that cash to finance growth and expansion with new marketing initiatives. And that leaves no cash to pay the consultants’ salaries doing the implementation throughout the year.

Without careful planning, the company might find itself cash-strapped midway through the project, potentially jeopardizing the project’s success and the company’s financial solvency.

Incorrect financial statements

Recording deferred revenue and keeping track of it can be complex, requiring strong accounting processes. Errors in tracking deferred revenue can lead to financial statement errors.

This, in turn, can mislead investors, creditors, and even regulatory bodies. In some cases, non-compliance with accounting standards and regulations can result in penalties, fines, and legal repercussions.

Customer service risks

Failure to record deferred revenue can easily cause a business to lose track of its commitments. This can lead to delays or failures in fulfilling customer orders, which is frustrating for them.

Customers expect businesses to honor their commitments. When a company fails to deliver on its promises due to poor management of deferred revenue, it erodes customer trust.

Deferred revenue FAQ

Is deferred revenue a good thing?

Although deferred revenue is a liability, it is not necessarily a bad thing. Businesses with deferred revenue can convert it to revenue after performing agreed-upon services or delivering products.

What is an example of deferred revenue?

Examples of deferred revenue include an annual gym membership paid in advance, a gift card purchase, or tickets to a future event, such as a concert or sporting event.

How is deferred revenue treated?

Deferred revenue is treated as a liability and is shown on a company’s balance sheet.

How do you record deferred revenue?

Deferred revenue creates an increase in your cash account and an increase in a deferred revenue account, which is a liability.

If Shopify is of interest and you'd like more information, please do make contact or take a look in more detail here.

Credit: Original article published here.